Summary Statistics for Empirical Distributions

empirical_stats.RdComputes the mean, standard deviation, skewness, kurtosis, Value-at-Risk (VaR) and Conditional Value-at-Risk CVaR) under flexible probabilities.

empirical_stats(x, p = NULL, level = 0.01)

Arguments

| x | A time series defining the scenario-probability distribution. |

|---|---|

| p | A probability vector. If |

| level | A number with the desired probability level. The default is

|

Value

A tibble with 2 columns and 6 rows.

Examples

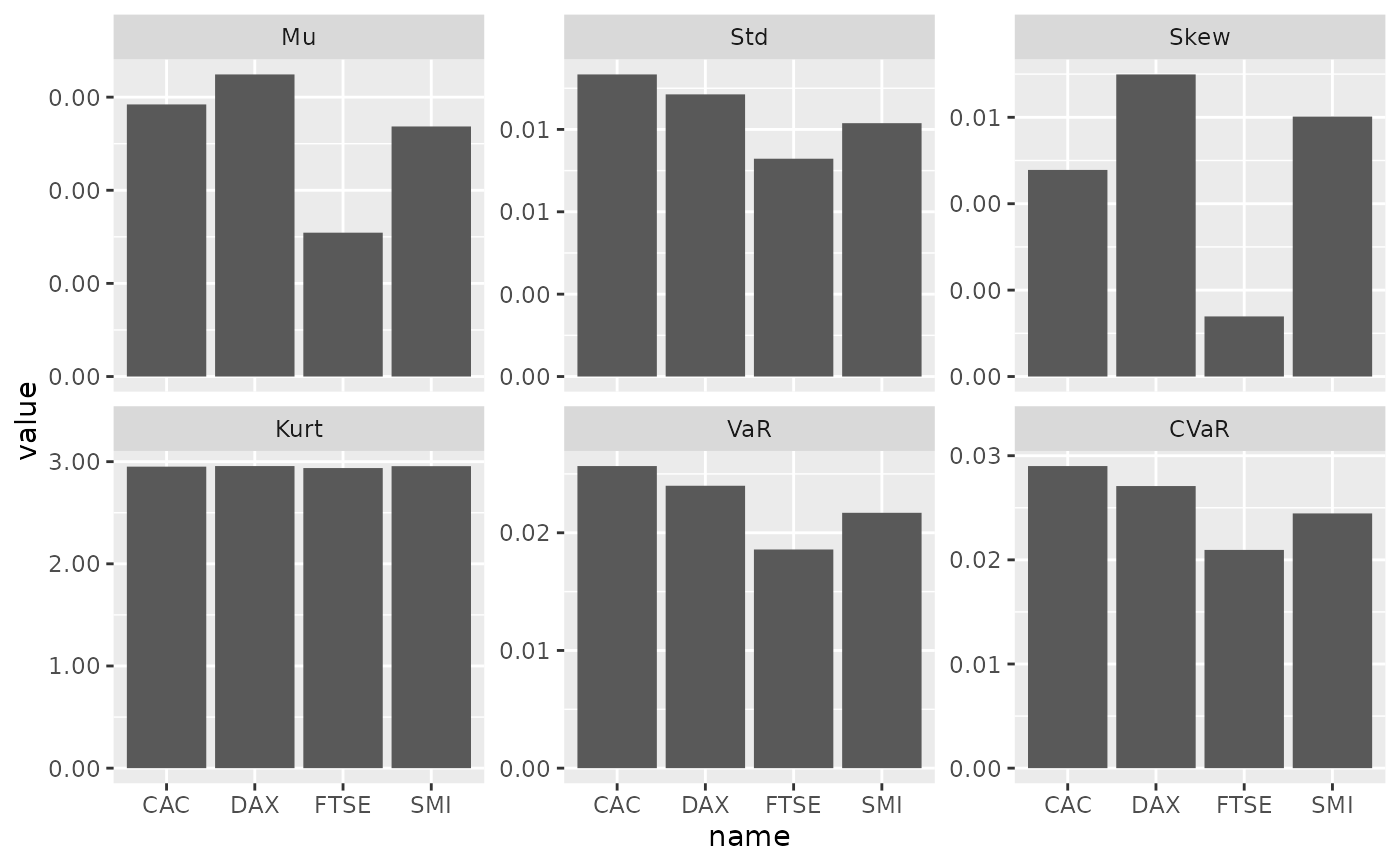

library(ggplot2) x <- diff(log(EuStockMarkets)) calm_market <- panic_copula(x = x, n = 1000, panic_prob = 0.00, dist = "normal") panic_market <- panic_copula(x = x, n = 1000, panic_prob = 0.20, dist = "normal") # Plot Calm market stats emp_calm <- empirical_stats(calm_market$simulation, p = calm_market$p) ggplot(emp_calm, aes(x = name, y = value)) + geom_col() + facet_wrap(~stat, scales = "free_y") + scale_y_continuous(labels = scales::number_format(accuracy = 0.01))# Plot Panic market stats emp_panic <- empirical_stats(panic_market$simulation, p = panic_market$p) ggplot(emp_panic, aes(x = name, y = value)) + geom_col() + facet_wrap(~stat, scales = "free_y") + scale_y_continuous(labels = scales::number_format(accuracy = 0.01))