Panic Copula

panic_copula.Rmd

library(cma)

library(dplyr, warn.conflicts = FALSE)

# stationarity - "invariance"

x <- matrix(diff(log(EuStockMarkets)), ncol = 4)

colnames(x) <- colnames(EuStockMarkets)

head(x)

#> DAX SMI CAC FTSE

#> [1,] -0.009326550 0.006178360 -0.012658756 0.006770286

#> [2,] -0.004422175 -0.005880448 -0.018740638 -0.004889587

#> [3,] 0.009003794 0.003271184 -0.005779182 0.009027020

#> [4,] -0.001778217 0.001483372 0.008743353 0.005771847

#> [5,] -0.004676712 -0.008933417 -0.005120160 -0.007230164

#> [6,] 0.012427042 0.006737244 0.011714353 0.008517217Assume there is a portfolio of stocks that is equally weighted on the indexes that appears in object x.

The main statistics of the P&L can be seen with empirical_stats():

empirical_stats(pnl)

#> # A tibble: 6 × 3

#> stat name value

#> <fct> <chr> <dbl>

#> 1 Mu base_pnl 0.000585

#> 2 Std base_pnl 0.00832

#> 3 Skew base_pnl -0.583

#> 4 Kurt base_pnl 7.83

#> 5 VaR base_pnl 0.0223

#> 6 CVaR base_pnl 0.0302The big question here is: how would the P&L statistics change in response to a massive sell-off?

To address this question we follow A New Breed for Copulas for Risk and Portfolio Management and model the market as a mixture of “calm” vs. “panic” distributions. For details on the full specification of this market, please, see the reference above.

# For the details on how the market is modeled, please, see the paper:

# "A New Breed for Copulas for Risk and Portfolio Management"

panic <- panic_copula(x, n = 50000, panic_cor = 0.97, panic_prob = 0.02, dist = "normal")

calm <- panic_copula(x, n = 50000, panic_cor = 0.00, panic_prob = 0.00, dist = "normal")We simulate 50.000 scenarios that matches the normal distribution exactly, with the sample counterparts of \(\mu\) and \(\sigma\).

In the first scenario we assume there is a 2% probability of panic, in which all the cross-correlations are equal to 0.97. We also model a “calm” scenario without changing the historical correlation structure.

For consistency, we continue with an equal-weight strategy for both simulations:

# Equal-Weight Portfolio Under the Panic Market

pnl_panic <- tibble::tibble(

pnl_panic = as.matrix(panic$simulation) %*% w

)

# Equal-Weight Portfolio Under the Calm Market

pnl_calm <- tibble::tibble(

pnl_calm = as.matrix(calm$simulation) %*% w

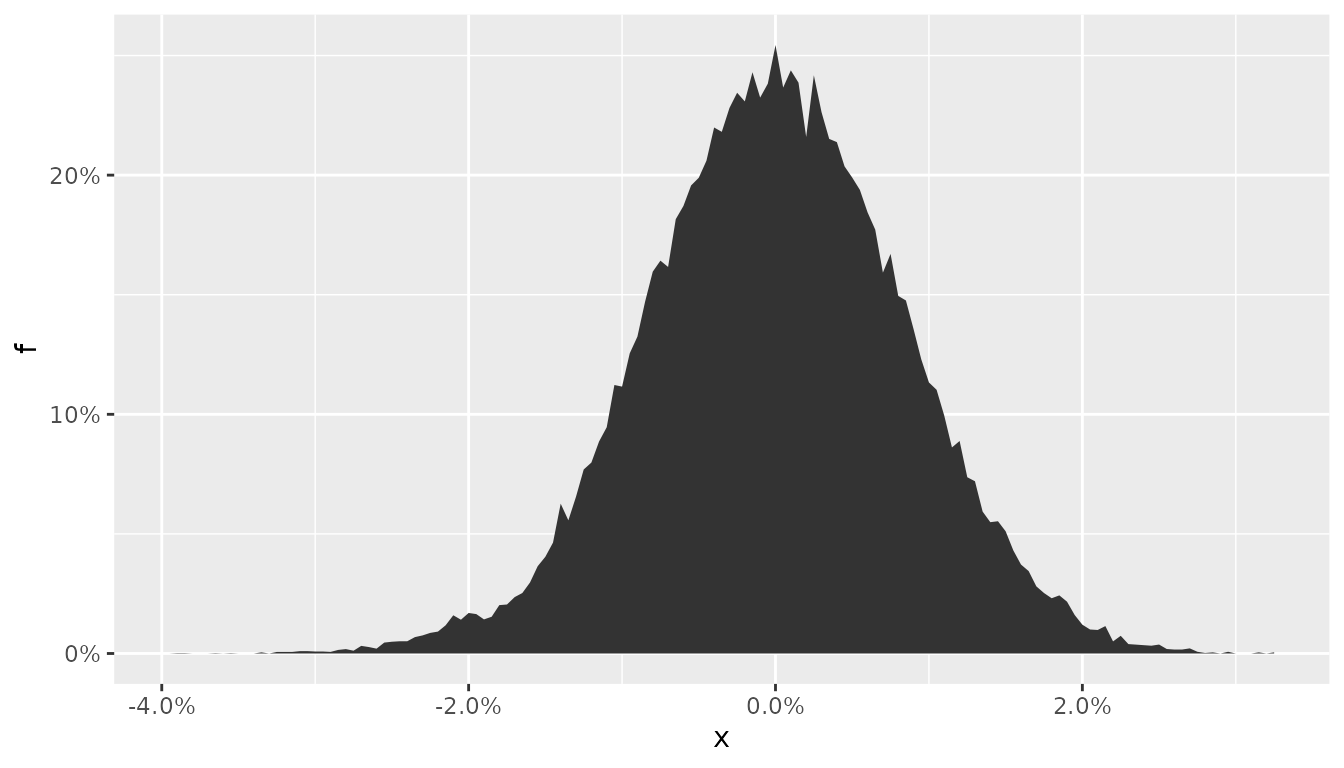

)The “panic” P&L can be seen with plot_panic_distribution():

# PnL under the Panic Regime

plot_panic_distribution(pnl_panic, panic$p, breaks = 200)

The new marginal distribution shows a hump shape format around -2%, which is a direct consequence of the panic. Nevertheless, the location and dispersion still matches the sample counterparts. The panic is hidden!

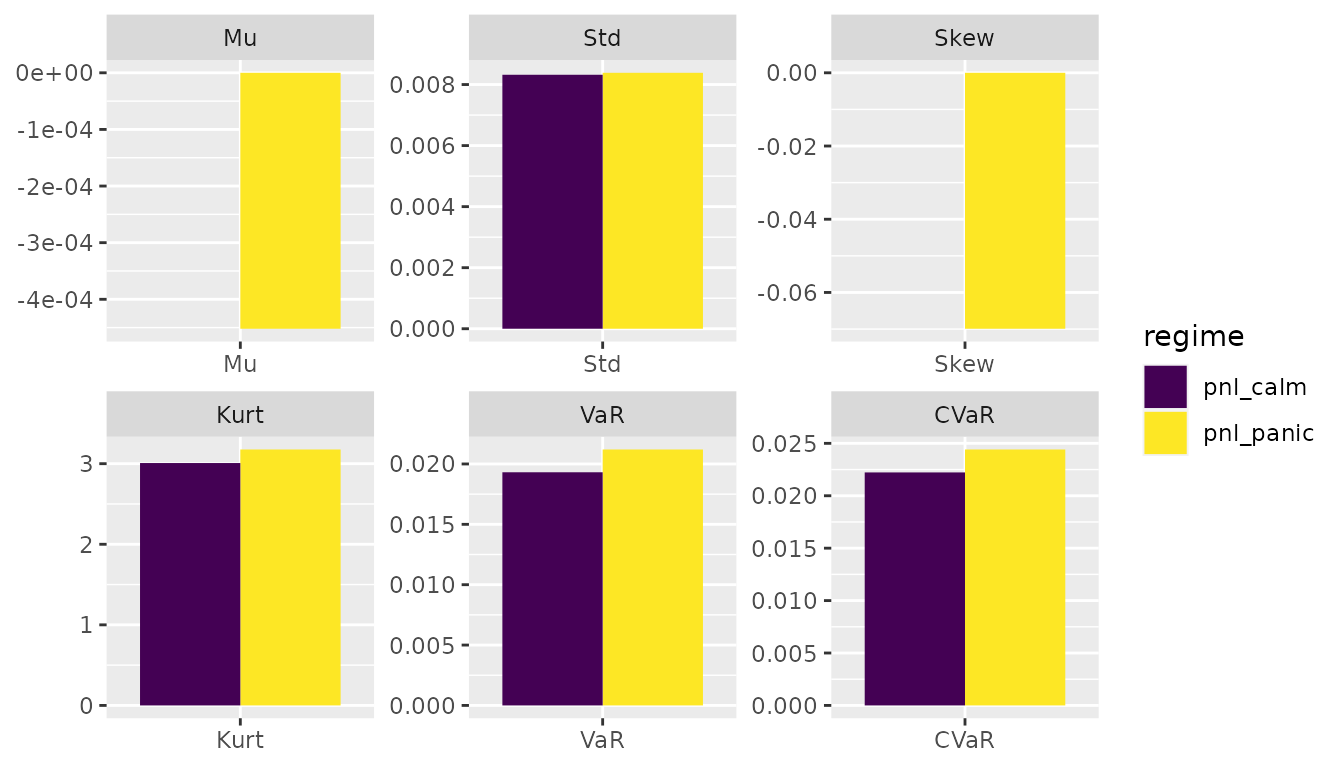

The full picture - with the similarities and differences - among these markets can be seen with help of ggplot2:

stats_panic <- empirical_stats(pnl_panic)

stats_calm <- empirical_stats(pnl_calm)

bind_rows(stats_panic, stats_calm) |>

ggplot2::ggplot(ggplot2::aes(x = stat, y = value, fill = name)) +

ggplot2::geom_col(position = "dodge") +

ggplot2::facet_wrap(~ stat, scales = "free") +

ggplot2::labs(x = NULL, y = NULL, fill = "regime") +

ggplot2::scale_fill_viridis_d()

While the location and dispersion doesn’t change, all the other metrics are twisted for markets that operate under multiple regimes. The objects stats_panic and stats_calm imply that a 2% probability of panic increases the kurtosis by 6% and VaR and CVaR by 10%.