DynamicStrategies is currently on the development stage.

Installation

Install the development version from github with:

# install.packages("devtools")

install.packages("DynamicStrategies")Example

library(DynamicStrategies)

library(ggplot2)

# Build a Convex Strategy

convex_strat <- simulate_strategy(strategy = "max_utility")

convex_strat

#> << Dynamic Strategy >>

#> time : 0 0.003968254 0.007936508 ... 0.4920635 0.4960317 0.5

#> portfolio_series : 10000 9774.044 9592.819 ... 13677.28 13556.93 13785.87

#> market_series : 10000 9546.501 9190.973 ... 17985.99 17666.63 18260.51

#> percentage_series: 0.5 0.5 0.5 ... 0.5 0.5 0.5

#> underlying_index : 18260.51 11529.34 9717.875 ... 25244.07 8463.544 12101.33

#> portfolio_value : 13785.87 10932.21 10040.53 ... 16220.87 9410.509 11207.85

# See the main statistics

extract_stats(convex_strat)

#> # A tibble: 6 x 2

#> stat value

#> <fct> <dbl>

#> 1 PnL 10628.

#> 2 Volatility 1505.

#> 3 Skewness 0.479

#> 4 Kurtosis 3.51

#> 5 VaR 2433.

#> 6 CVaR 2736.

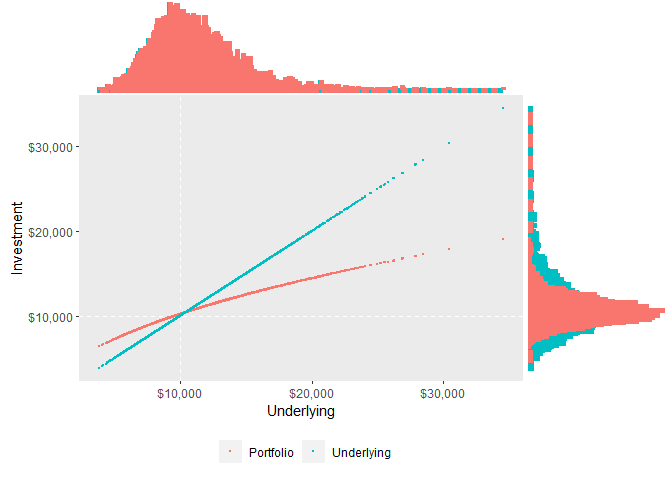

# See the P&L simulation

autoplot(convex_strat)

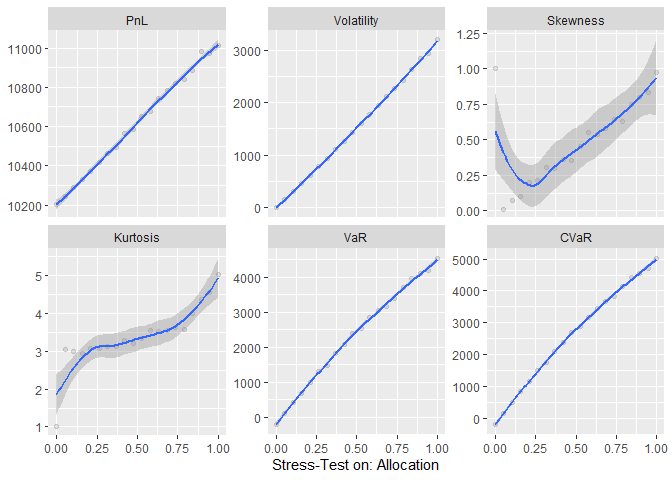

# Stress-Test a parameter

plot_sensivities(strategy = convex_strat, variable = "allocation", from = 0, to = 1, size = 20)

References

Attilio Meucci (2021). Review of Dynamic Allocation Strategies (https://www.mathworks.com/matlabcentral/fileexchange/28384-review-of-dynamic-allocation-strategies), MATLAB Central File Exchange. Retrieved September 5, 2021.

Meucci, Attilio, Review of Dynamic Allocation Strategies: Utility Maximization, Option Replication, Insurance, Drawdown Control, Convex/Concave Management (July 7, 2010). Available at SSRN: https://www.ssrn.com/abstract=1635982